cafeteria plan

Making Plan Changes During the COVID-19 Pandemic

Needless to say, these last several weeks have created challenging times for a significant number of employers. Stay-at-home orders and other impacts from the COVID-19 (Coronavirus) pandemic have put many employers in a position where they must make sudden health plan and benefit changes.

Many insurance carriers are offering up a limited time special enrollment period due to the COVID-19 (Coronavirus) pandemic. Call it a midyear open enrollment period if you will. No qualifying event is necessary to enroll in the group health plan. Many insurance carriers (at the discretion of the employer) are allowing employees to join the group health plan if they waived coverage during the employer’s typical open enrollment period. This comes as good news for many employees.

Simple Cafeteria Plans were created by the Affordable Care Act (ACA) and have been an option for eligible employers since 2011. This type of plan provides eligible employers with an automatic pass for many of the non-discrimination tests that apply to Cafeteria Plans and its component benefits. This is the primary difference between a Simple Cafeteria Plan and other more traditional Cafeteria Plans.

Many employers offer a cash payment to employees who waive health insurance coverage. These cash payments are always taxable to employees who waive health insurance coverage, but did you know employees who elect the health insurance coverage may be subject to paying taxes on the cash payment that they didn’t receive?

Wait! What?

Premium Only Plans (POP) can generally be defined as a type of Cafeteria Plan where the only pre-tax benefit available to employees are for those of insurance premiums. Now, whenever non-taxable benefits are involved, the IRS will usually have some strict rules in place that must be followed. For Cafeteria Plans, these are referred to as non-discrimination rules, and these rules are in place to ensure the plan doesn’t discriminate in favor of highly compensated and/or key employees.

What happens to Health and Dependent Care FSAs when a merger or acquisition occurs?

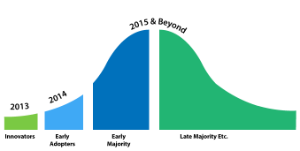

After nearly thirty years of lobbying the “Use-It-or-Lose-It” rule has been changed. Now the option is left to you, the plan sponsor, whether or not it is the right thing to implement for your company. Let’s take a look at some of the scenarios and helpful tips for the healthcare flexible spending account (FSA) rollover option in terms of an adoption lifecycle (a model that shows the trend of acceptance to a new concept over time).

As tax season comes to a close, you might be wondering how to save more next year. Flexible Spending Accounts (FSAs) are a great tool that allows you and your employees to save on healthcare and dependent care expenses. Celebrating 25 years as a trusted benefits administrator, we have done the math to help you visualize your potential savings with our FlexFSA® product:

Benefits Buzz

Enter Your Email